A decade ago, Tesla looked like a bold bet on a niche technology. Today, it anchors the global conversation about electrification, autonomy, energy storage, and the software-defined car. For investors and traders alike, the central question is no longer whether Tesla will matter in 2030—it’s how much and in which lines of business. This article takes a professional, friendly look at Tesla’s journey so far and what may shape the next five years, including a balanced 2025 forecast and three scenario paths for 2026–2030. You’ll also find a concise list of pros and cons and a larger FAQ to help you stress-test assumptions.

Note: The projections presented here are scenario ranges for planning and education—not guarantees. Markets evolve, and Tesla’s path depends on execution, policy, capital markets, and competition.

Tesla: Company History

Tesla was founded in 2003 with a mission that seemed almost radical at the time: to prove that electric vehicles could compete head-to-head with gasoline cars not only on efficiency but also on performance, desirability, and everyday practicality. At the turn of the millennium, the automotive industry was still deeply tied to the internal combustion engine, with electric cars often dismissed as slow, unattractive, and short-ranged. Tesla’s founders believed that this perception was outdated, and that advances in battery technology and software could redefine the category.

The company’s first vehicle, the Roadster, was introduced in 2008 and targeted a narrow but symbolic niche: the high-end sports car market. By choosing this entry point, Tesla aimed to demonstrate that electric cars could be fast, stylish, and aspirational. The Roadster was not meant to be a mass-market car; rather, it was designed as a proof of concept and as a brand statement. It attracted early adopters, drew media attention, and created the foundation for investor confidence, while also helping Tesla raise the capital needed to move toward larger ambitions.

Building on that momentum, Tesla laid out a clear roadmap to gradually bring electric vehicles to broader audiences. The Model S, introduced in 2012, was a luxury sedan that redefined expectations of range and performance for EVs. It was followed by the Model X, a premium SUV, in 2015, which extended the product line and introduced innovations in design and safety. The company then pivoted toward affordability with the Model 3 in 2017, its first mainstream vehicle aimed at higher production volumes. The Model Y, a compact crossover released in 2020, quickly became one of the company’s best-selling models, appealing to families and a wider demographic of drivers.

Unlike traditional carmakers that relied on dealership networks, Tesla adopted a direct-to-consumer model. Customers could order vehicles online and have them delivered directly, creating a streamlined sales process and giving the company greater control over pricing, branding, and customer experience. Tesla also invested heavily in vertical integration, choosing to build many of its components in-house and to operate its own gigafactories. This strategy was paired with a strong focus on battery research, energy density improvements, and scalable manufacturing techniques.

Software was always positioned as a core part of Tesla’s identity. Over-the-air updates allowed cars to receive new features, improved efficiency, and safety enhancements long after purchase, giving owners a sense that their vehicle could evolve over time. This approach created a connection between the company and its customer base that went beyond the initial sale, establishing a dynamic relationship uncommon in the automotive world.

As production scaled and the vehicle business matured, Tesla began to diversify. It expanded into energy storage with products for homes, businesses, and utility-scale projects, linking clean energy generation with efficient storage solutions. The company also began developing advanced driver-assistance systems, laying the groundwork for full autonomy as a potential long-term growth driver. More recently, Tesla has ventured into new frontiers such as humanoid robotics and artificial intelligence, signaling an ambition to extend its influence far beyond cars.

Today, Tesla can no longer be defined simply as an automaker. It has grown into a multi-segment technology and energy enterprise that spans vehicles, batteries, software, grid solutions, and emerging fields like robotics. Its history is marked by bold bets, significant execution risks, and periods of volatility, but also by a consistent ability to challenge assumptions and reshape industries. This combination of innovation, scale, and unpredictability makes Tesla one of the most closely watched companies in the global market.

Tesla’s Stock Market History

Tesla’s stock market history is a vivid illustration of how investor sentiment can shift dramatically when bold promises begin to align with tangible results. At its core, Tesla’s journey reflects the way financial markets weigh not just present performance but also future possibilities. For years after the company’s IPO in 2010, Tesla was treated with caution, even skepticism, by large parts of Wall Street. Many analysts doubted whether the company could achieve mass production, reach profitability, or sustain demand for electric vehicles in a world dominated by gasoline-powered cars.

The stock’s early years were characterized by bursts of enthusiasm followed by equally sharp pullbacks. Whenever Tesla achieved a significant milestone—such as the successful launch of the Model S in 2012, or breakthroughs in battery development—its share price would climb, sometimes dramatically. Yet each surge was often followed by a correction as skeptics pointed to production bottlenecks, cash burn, or questions about the scalability of its business model. This volatility defined Tesla as a high-risk, high-reward stock in its first decade of trading.

The real inflection point came around 2019 and 2020. After years of heavy investment, Tesla achieved consistent profitability and began to scale production in a way that silenced many critics. The ramp-up of the Model 3 and the opening of new gigafactories provided evidence that Tesla could compete not only on technology but also on manufacturing capacity. At the same time, the broader market was beginning to assign higher valuations to growth companies, particularly those linked to sustainability and clean energy. Tesla benefited from this re-rating, and the stock’s meteoric rise during 2020 captured global attention.

This phase saw Tesla become one of the world’s most valuable companies, joining the S&P 500 and surpassing the combined market capitalizations of many traditional automakers. The rally was fueled not only by financial results but also by the belief that Tesla’s future lay in areas beyond vehicles—robotaxis, software subscriptions, and energy solutions. Investors began to price in optionality, treating Tesla less like a car company and more like a technology platform with multiple growth levers.

Yet the journey was far from linear. After reaching new highs, Tesla’s stock experienced periods of sharp correction. These declines often coincided with macroeconomic headwinds such as rising interest rates, inflation concerns, and shifts in investor appetite for risk. At the company level, pricing adjustments, supply chain challenges, and intensifying competition also played a role. Each correction served as a reminder that while Tesla has a compelling long-term story, its execution risks and sensitivity to external factors remain significant.

Looking at the chart of Tesla’s stock price from 2010 to 2025, one can see the unmistakable long-term upward arc punctuated by frequent volatility. It is this volatility that makes Tesla particularly interesting for traders. The stock has a history of delivering multi-quarter rallies when sentiment turns positive, only to reverse sharply when deliveries fall short, margins compress, or headlines raise fresh concerns. For active market participants, this pattern creates both opportunity and risk, requiring a disciplined approach to position sizing and risk management.

Chart: Tesla Stock Price History (2010–2025)

.webp)

This figure provides a visual representation of Tesla’s long-term trajectory and highlights the dramatic transformation in market perception over the past fifteen years.

What stands out is not just the scale of Tesla’s rise but the character of its moves. Tesla is not a stock that drifts quietly upward or downward. Instead, it reacts strongly to catalysts, reflecting how deeply investor expectations are tied to execution milestones. This characteristic is unlikely to change as we approach 2030, meaning Tesla will probably continue to be a stock defined by powerful rallies and equally forceful corrections, offering both challenges and opportunities for traders and investors.

Key Factors Influencing Tesla Stock Price by 2030

Autonomy and the Robotaxi Opportunity

Tesla’s autonomy roadmap, culminating in potential robotaxi services, is the most controversial driver of long-term value. If software and fleet operations scale safely and gain regulatory acceptance, robotaxis could introduce high-margin, recurring revenue that is less cyclical than vehicle sales. The flip side is clear: delays or technical bottlenecks would push monetization to the right and compress multiples.

What to watch: the pace of supervised autonomy improvements, regulator feedback, the geography of pilot programs, and real-world utilization metrics if/when paid rides expand.

Energy Storage and Grid Services

The Energy segment—utility-scale storage, commercial solutions, and software—has matured from an experiment into a credible growth pillar. Demand for grid-balancing and storage solutions continues to increase as renewables grow. If Energy sustains healthy margins and attaches software/service revenue, it can smooth earnings through auto cycles.

What to watch: annual deployment growth, gross margin trajectory, backlog, and software attach rates.

Vehicle Program, Cost Structure, and Manufacturing Innovation

Cost leadership is strategic. Tesla’s work on cell technology, structural pack designs, gigacasting, drive units, and simplified architectures aims to drive down vehicle cost while preserving functionality. A successful next-gen platform (lower cost, high volume) could defend share against aggressive competition, especially in price-sensitive markets.

What to watch: factory utilization, learning-curve effects, and the launch cadence of refreshed or next-gen vehicles.

Competition: Global, Relentless, and Getting Smarter

EV competition has intensified across segments and geographies. Pricing power ebbs and flows with incentives, logistics, FX, tariffs, and the rate environment. Competitors are learning fast in software and manufacturing—especially in Asia—putting pressure on Tesla to keep its innovation velocity high.

What to watch: price changes, wait times, incentive structures, and share trends in China, the U.S., and Europe.

Policy, Incentives, and Macroeconomics

Policy affects demand and margins. Incentives can accelerate adoption; their removal can slow it. Tariffs and local content rules reshape supply chains and market access. Meanwhile, rates and liquidity conditions swing valuation multiples, especially for growth names.

What to watch: changes in EV credits, local manufacturing rules, tariff regimes, and the broader rate cycle.

Capital Allocation and Optionality

Investors also weigh R&D intensity, buybacks vs. reinvestment, and optional bets (robotics, energy software, insurance, etc.). Clearer disclosures and milestones can reduce uncertainty discounts.

Bottom line: By 2030, Tesla’s stock will reflect not just vehicle volume but the mix of revenues: how much comes from services and software vs. hardware—and how consistently those earnings arrive.

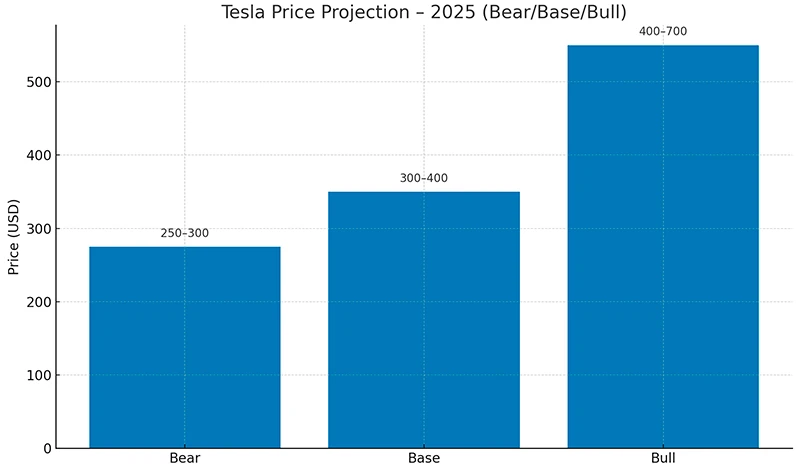

Tesla Price Forecast: 2025

To help set near-term expectations, here is a balanced scenario framework for 2025. The point is not to pinpoint a number but to map conditions that could shift the stock within a range.

Scenario Ranges (2025)

- Bear: $250–$300

Softer EV demand in key regions; prolonged pricing pressure; slower Energy margin expansion; autonomy progress mostly limited to small pilots.

- Base: $300–$400

Stabilizing demand with selective pricing actions; incremental cost wins; Energy unit growth; early but meaningful steps toward monetization of software/autonomy.

- Bull: $400–$700

Stronger delivery cadence; Energy scaling with attractive margins; rising confidence in autonomy economics; improved sentiment toward growth equities.

Tesla Price Projection — 2025 Chart

Trading note (CFDs): On NordFX, traders can express short-term views on Tesla via CFDs—going long if they expect strength or short if they expect weakness. CFD trading involves leverage, which magnifies both potential gains and losses. Always size positions responsibly.

Opportunities and Challenges for Tesla in 2026 to 2030

The Big Opportunities

The second half of the decade may give Tesla the chance to prove that its bold projects can scale into lasting businesses. One of the clearest opportunities is robotaxi commercialization. Limited pilots in the mid-2020s could, if successful, evolve into wider roll-outs across key cities. Even a measured adoption would help Tesla diversify its revenue mix and introduce service-style income that is less cyclical than car sales.

Energy storage and software services also stand out as a growth engine. As demand for renewable energy grows, Tesla is well positioned with its Megapack systems and grid solutions. If margins improve and software becomes a larger part of the package, the energy division could provide steady earnings that balance out the volatility of vehicle sales.

Manufacturing innovation remains another opportunity. By refining its next-generation platform and factory processes, Tesla can lower production costs, defend market share, and maintain profitability despite price competition. In parallel, the expansion of related services—insurance, charging, and fleet management—may enhance customer loyalty and increase lifetime value.

The Non-Trivial Challenges

The biggest obstacle remains the uncertainty surrounding autonomy. Even if the technology works, regulatory approval and public acceptance will determine the pace of adoption. Any setbacks could delay or reduce expected revenue streams.

Another challenge is intensifying competition. Rivals across the U.S., Europe, and especially Asia are expanding aggressively, which increases pressure on Tesla’s pricing and margins. To maintain leadership, Tesla must stay ahead in both innovation and cost efficiency.

Execution complexity is also a risk. Running multiple businesses—vehicles, energy, autonomy, and emerging projects—requires careful capital allocation and management focus. Missteps in coordination could slow progress. Finally, narrative-driven volatility will continue. Tesla’s valuation depends heavily on expectations, which means headlines about deliveries, margins, or autonomy can drive sharp swings in sentiment.

Investor takeaway: The 2026–2030 horizon will likely be shaped by many smaller steps rather than a single turning point. Each success or setback in scaling autonomy, expanding energy, or managing costs could tip Tesla closer to its bull or bear path by the end of the decade.

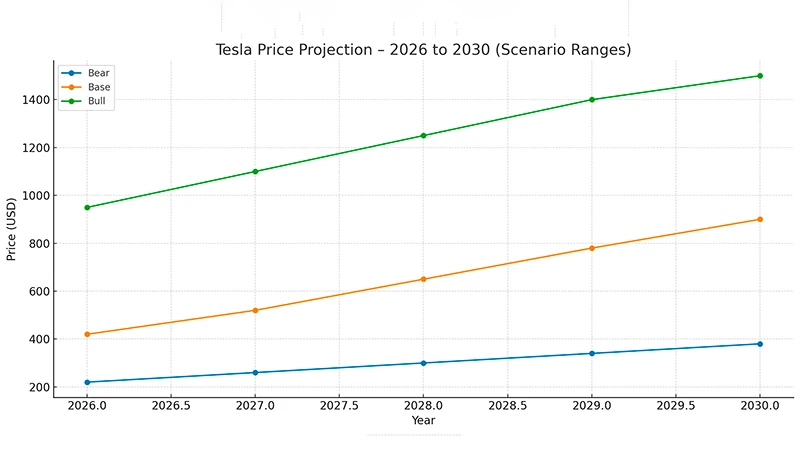

Analytical Tesla Stock Price Forecast for 2026 to 2030

Below is a scenario map to frame what 2030 could plausibly look like. Values are illustrative ranges designed for planning and risk-management exercises.

Bear Case

- Price Range by 2030: $200–$400

Narrative: Autonomy remains limited to narrow use-cases; Energy grows but at modest margins; competition compresses auto profits; valuation centers on a solid automaker plus a slower-burn energy arm.

Milestones that would bias toward this path: frequent delays in autonomy milestones; elevated price competition; weak incentives; margin compression that persists beyond two model refresh cycles.

Base Case

- Price Range by 2030: $400–$900

Narrative: Autonomy generates revenue in a growing but still selective set of geographies; Energy becomes a durable contributor with healthier margins; manufacturing efficiency offsets some price pressure; valuation reflects a balanced portfolio of auto + energy + early services.

Milestones to support this: multi-city autonomy monetization, year-over-year Energy deployment growth with margins trending higher, visible factory learning-curve effects, and a next-gen platform launch that meaningfully reduces unit cost.

Bull Case

- Price Range by 2030: $900–$1,500+

Narrative: Robotaxis scale with compelling unit economics; Energy achieves global relevance with attractive software/services attach; auto volumes regain momentum with a cost-efficient platform; valuation re-rates toward a services-heavy tech-energy hybrid.

Milestones to watch: multiple countries allowing paid autonomy operations, software revenue per vehicle rising, Energy margins consistently outpacing auto, and strong free-cash-flow generation.

Tesla Price Projection — 2026 to 2030

Investing in Tesla: Pros and Cons

Pros

- Powerful optionality beyond autos: autonomy, energy, software, and services could reshape the earnings mix by 2030.

- Scale and learning curves: a global manufacturing footprint and platform simplification can drive unit cost lower over time.

- Brand and ecosystem: strong consumer mindshare, integrated charging, and software updates reinforce loyalty and differentiation.

- Potential for higher-quality revenue: software and services can reduce cyclicality relative to pure hardware businesses.

Cons

- Execution risk in autonomy: technical, regulatory, and safety hurdles could delay or limit monetization.

- Pricing pressure and competition: aggressive rivals, especially in Asia, can compress margins and challenge share.

- Policy sensitivity: credits, tariffs, and local-content rules can shift quickly, affecting demand and cost.

- Narrative-driven volatility: when optionality dominates, sentiment swings can be large and fast—both ways.

How traders use this:

On NordFX, Tesla CFDs allow flexible positioning around catalysts (deliveries, updates, macro data). You can go long to express optimism or short to hedge or bet on weakness. Pair Tesla with correlated or diversifying assets to manage portfolio risk. Always remember that leverage magnifies outcomes.

FAQ

1. Does Tesla pay a dividend?

No. The company historically reinvests cash into growth initiatives.

2. How many times has Tesla split its stock?

Twice in recent years. Splits do not change the company’s value; they change share count and price per share.

3. What exactly is a robotaxi and why does it matter?

A robotaxi is an autonomous ride-hailing service. If it scales, Tesla could earn recurring, higher-margin revenue per vehicle, potentially lifting valuation multiples.

4. What are the biggest risks to the autonomy thesis?

Regulatory approvals, safety performance in diverse real-world conditions, data quality, and the ability to scale across cities and countries.

5. What is Tesla Energy and why do investors care?

It’s the storage and grid-services business (plus software). It can diversify revenue away from auto cycles and may carry attractive margins if software attach rates rise.

6. How do interest rates affect Tesla’s valuation?

Higher rates typically compress growth-stock multiples. Lower rates tend to be supportive, all else equal.

7. Why does pricing move so much on delivery or margin headlines?

Tesla trades on both current results and future optionality. Small changes in trajectory can cause large repricings.

8. Is a lower-priced next-gen vehicle essential by 2030?

It’s very helpful. A cost-efficient platform helps defend share and soften pricing pressure while supporting scale.

9. Could Tesla’s stock do well even if robotaxis take longer?

Yes—if Energy grows strongly with healthy margins, and if auto volumes remain solid with cost advantages.

10. Why are scenario ranges so wide?

Because a meaningful share of long-term value depends on timelines and regulatory outcomes that are inherently uncertain.

11. How do tariffs and incentives factor into the outlook?

They influence demand, pricing, and supply chains. Shifts can be abrupt, which is why scenario planning is useful.

12. What role does software play outside autonomy?

Software can enhance in-car experiences, enable paid features, and support Energy and fleet operations—all potential margin levers.

13. Is Tesla still a “car company” by 2030?

It will still sell vehicles, but the more important question is the mix: what fraction of revenue and profit comes from services and software?

14. How can I trade Tesla on NordFX?

You can trade CFDs on Tesla (TSLA) through NordFX platforms (MetaTrader 4/5). CFDs let you go long or short and use leverage. Please understand the risks before trading.

Conclusion

Tesla’s 2030 outcome hinges on more than unit sales. The next five years will test whether autonomy and Energy can become scalable, profitable pillars that complement vehicle hardware. That mix—plus policy, rates, and competition—will drive how investors value Tesla at decade’s end. For traders, the stock’s volatility is both a risk and an opportunity; the key is to have a framework, manage position size, and stay flexible as information changes.

If you’re exploring trading opportunities around Tesla’s catalysts, NordFX provides access to Tesla CFDs on MetaTrader 4 and MetaTrader 5, enabling both long and short strategies with efficient execution and risk controls at your fingertips.

Disclaimer: These materials are not an investment recommendation or a guide for working on financial markets and are for informational purposes only. Trading on financial markets is risky and can lead to a complete loss of deposited funds.

Kembali Kembali