EUR/USD: อัตราลดลง, ดอลลาร์ตก

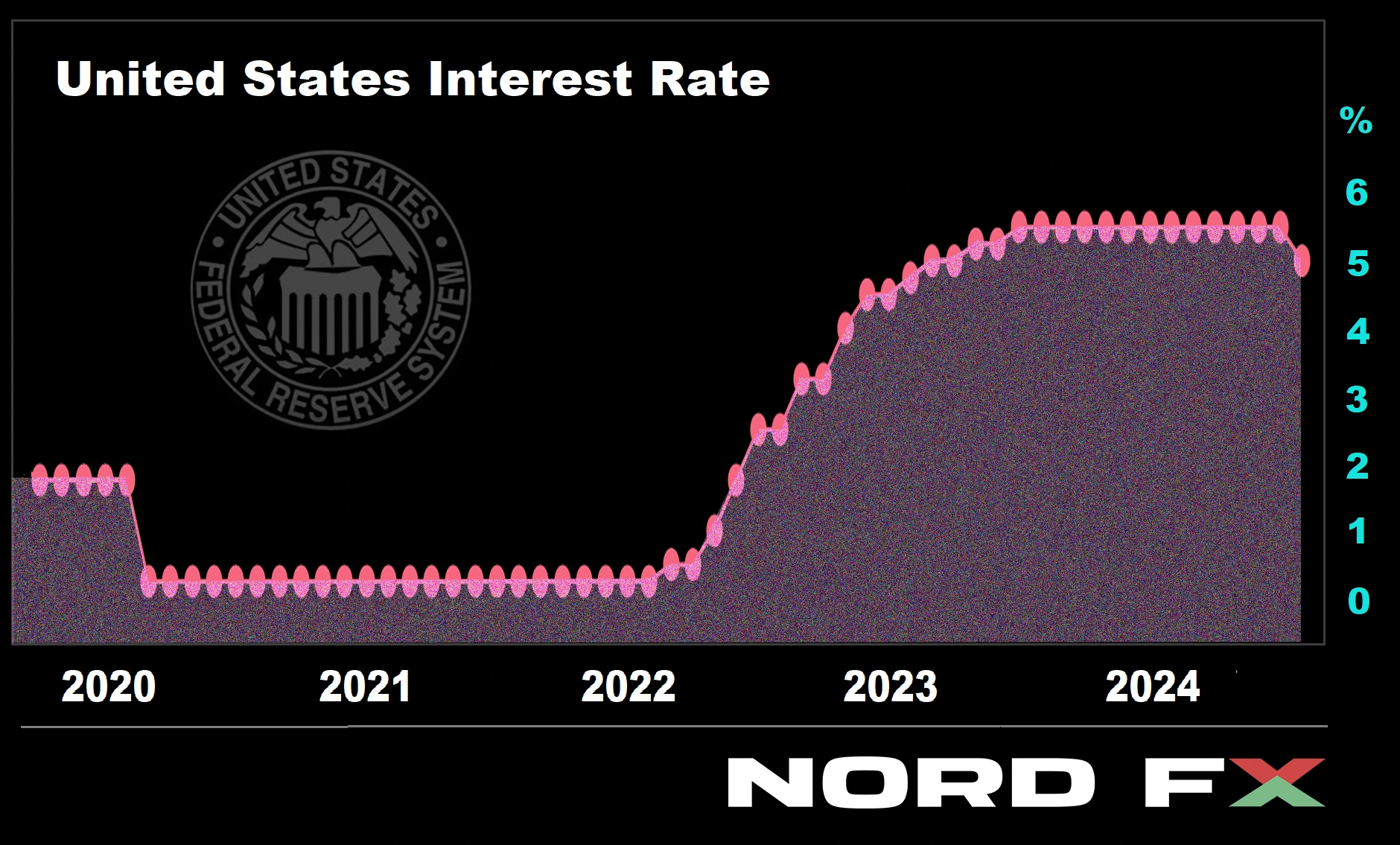

● ระบบธนาคารกลางสหรัฐ (Fed) ได้ประกาศการตัดสินใจเกี่ยวกับอัตราดอกเบี้ยมาตรฐานหลังจากการประชุมสองวันที่จัดขึ้นในวันที่ 17-18 กันยายน ความน่าตื่นเต้นนั้นอยู่ที่การลดอัตราดอกเบี้ย — ไม่ว่าจะเป็น 25 จุดพื้นฐาน (bps) ตามปกติหรือจะมากเป็นสองเท่า ก่อนการประชุม ตลาดคาดการณ์ว่าโอกาสของการลดลง 25 bps อยู่ที่ 45% และโอกาสของการลดลง 50 bps อยู่ที่ 55% ในที่สุด ครั้งแรกในรอบสี่ปี ธนาคารกลางเลือกที่จะลดอัตราดอกเบี้ยลงครึ่งเปอร์เซ็นต์ทันที: จากระดับสูงสุดในรอบ 23 ปีที่ 5.50% เป็น 5.00%.

● ควรสังเกตว่าการลดอัตราดอกเบี้ยครั้งใหญ่เช่นนี้มักจะถูกนำมาใช้ในช่วงเริ่มต้นของนโยบายการเงินแบบผ่อนคลาย (QE) โดย Fed และจะใช้เฉพาะในสถานการณ์วิกฤติเท่านั้น ตัวอย่างเช่นในศตวรรษนี้ มีเหตุการณ์เช่นนี้เกิดขึ้นในปี 2001 (หลังจากการโจมตีเวิลด์เทรดเซ็นเตอร์ในนิวยอร์ก), ในปี 2007 (ช่วงเริ่มต้นของวิกฤตเศรษฐกิจ), และในปี 2020 (ช่วงการระบาดของ COVID-19) อย่างไรก็ตาม เหตุการณ์วิกฤติอย่างนี้ยังไม่เกิดขึ้นในปัจจุบัน ดังนั้นเหตุใดธนาคารกลางอเมริกาจึงตัดสินใจเช่นนี้?

นักวิเคราะห์บางคนอธิบายว่า Fed ล่าช้าในการลดอัตราดอกเบี้ยในเดือนกรกฎาคมและตอนนี้พยายามที่จะตามให้ทัน (โปรดจำไว้ว่าสมาชิกหลายคนของคณะกรรมการ FOMC [Federal Open Market Committee] พร้อมที่จะเริ่มลดอัตราดอกเบี้ยในช่วงกลางฤดูร้อน) ประธาน Fed เจอโรม พาวเวลล์ ไม่เห็นด้วยกับแนวคิดที่ว่าเป็นการล่าช้า แต่เขายอมรับว่าหากข้อมูลตลาดแรงงานในเดือนกรกฎาคมออกมาก่อนหน้าการประชุม FOMC แทนที่จะออกมาหลังจากนั้น การตัดสินใจอาจแตกต่างออกไป

การประชุมในเดือนกันยายนนี้ยังมีความโดดเด่นเนื่องจากเป็นครั้งแรกตั้งแต่ปี 2005 ที่การตัดสินใจของ Fed ไม่เป็นเอกฉันท์ หนึ่งในสมาชิก FOMC 12 คนคือ Michelle Bowman ได้ออกมาเสนอให้ลดอัตราดอกเบี้ยเพียง 25 bps แทนที่จะเป็น 50 bps

● การพยากรณ์ทางเศรษฐกิจที่อัปเดตของ Fed หลังการประชุมในวันที่ 17-18 กันยายน บ่งบอกถึงอัตราเงินเฟ้อที่ลดลงเร็วขึ้นและอัตราการว่างงานที่สูงขึ้น เจอโรม พาวเวลล์ เรียกสิ่งนี้ว่าเป็น "การเปลี่ยนแปลงสมดุลความเสี่ยง"

ตามการพยากรณ์ใหม่ อัตราเงินเฟ้อ (ดัชนี PCE) ในปีนี้จะอยู่ที่ 2.3% (การพยากรณ์ในเดือนมิถุนายนคือ 2.6%) ปีหน้าจะอยู่ที่ 2.1% (เดือนมิถุนายนคือ 2.3%) และในที่สุดในปี 2026 อัตราเงินเฟ้อจะลดลงไปยังเป้าหมายที่ 2.0% (ไม่มีการเปลี่ยนแปลง) ในปี 2027 และปีต่อๆ ไป อัตราเงินเฟ้อจะคงที่ที่ระดับเป้าหมาย

สำหรับการพยากรณ์การว่างงานในสหรัฐฯ ได้ถูกปรับขึ้นจาก 4.0% เป็น 4.4% ในปี 2024 และในปี 2025 คาดว่าจะคงที่ที่ 4.4% (เดือนมิถุนายนคือ 4.2%) และในปี 2026 คาดว่าจะลดลงเหลือ 4.3% (เดือนมิถุนายนคือ 4.1%) Fed คาดการณ์ว่าในปี 2027 และปีต่อไปอัตราการว่างงานจะคงที่ที่ 4.2%

การพยากรณ์การเติบโตของ GDP ในสหรัฐฯ สำหรับปี 2024 ถูกปรับลดลงจาก 2.1% เป็น 2.0% โดยคาดว่าจะมีอัตราเดียวกันสำหรับปี 2025-2027 ซึ่งสูงกว่าการเติบโตเฉลี่ยในระยะยาวที่ 1.8%

● นอกจากนี้ ธนาคารกลางยังได้ประกาศว่าจะมีการลดอัตราดอกเบี้ยอย่างต่อเนื่อง อย่างไรก็ตาม เนื่องจากการเปลี่ยนแปลงในการพยากรณ์เงินเฟ้อและตลาดแรงงาน แนวโน้มการลดอัตราดอกเบี้ยได้ถูกปรับให้อ่อนลงอย่างมาก ดังนั้น Fed คาดว่าอัตราดอกเบี้ยจะอยู่ที่ 4.5% ภายในสิ้นปีนี้ (อาจจะลดลงอีกสองครั้ง: ในเดือนพฤศจิกายนและธันวาคม ครั้งละ 25 bps) ในระยะเวลาหนึ่งปี คาดว่าอัตราดอกเบี้ยจะอยู่ที่ 3.4% และในปีต่อไปจะอยู่ที่ 2.9%

สิ่งสำคัญที่ต้องเข้าใจคือ การพยากรณ์เหล่านี้สามารถ (และจะ) เปลี่ยนแปลงได้ขึ้นอยู่กับสถานการณ์ทางภูมิรัฐศาสตร์ทั่วโลกและสถานการณ์ภายในสหรัฐฯ ตัวอย่างเช่น ผู้เชี่ยวชาญคาดว่า หากโดนัลด์ ทรัมป์ กลับเข้าสู่ทำเนียบขาว อาจทำให้เกิดการขาดดุลงบประมาณที่เพิ่มขึ้นอย่างมาก ซึ่งอาจทำให้การดำเนินนโยบาย QE ช้าลงอย่างมาก

● สำหรับเงินยูโร สกุลเงินยุโรปได้รับการสนับสนุนจากคำแถลงของเจ้าหน้าที่ระดับสูงของสหภาพยุโรปเมื่อเร็ว ๆ นี้ ตัวอย่างเช่น รองประธาน ECB หลุยส์ เดอ กินดอส กล่าวเมื่อสัปดาห์ที่แล้วว่า “เรายังคงเปิดประตูไว้ […] และในเดือนธันวาคมเราจะมีข้อมูลมากกว่าในเดือนตุลาคม” คำพูดเหล่านี้ชี้ให้เห็นอย่างชัดเจนว่าธนาคารกลางยุโรปไม่มีแผนที่จะตัดสินใจเรื่องอัตราดอกเบี้ยจนกว่าจะถึงเดือนธันวาคม สมาชิกสภาผู้ว่าการ ECB และผู้ว่าการธนาคารลิทัวเนีย เกดีมีนาส ชิมคุส ก็ได้ลดความคาดหวังของตลาดเมื่อวันอังคารที่ 17 กันยายน โดยกล่าวว่า “โอกาสที่อัตราดอกเบี้ยจะลดลงในเดือนตุลาคมนั้นต่ำมาก” “ในเดือนตุลาคม เราจะไม่มีข้อมูลใหม่มากนัก และเศรษฐกิจก็กำลังพัฒนาไปตามการคาดการณ์” เขากล่าวเสริม

ขณะนี้ อัตราดอกเบี้ยมาตรฐานของ ECB อยู่ที่ 3.65% ดังนั้นหากความแตกต่างระหว่างอัตราดอกเบี้ยของ Fed และ ECB (และธนาคารกลางอื่น ๆ) แคบลงภายในสิ้นปีนี้และตลอดทั้งปีหน้า จะกดดันดอลลาร์ ในขณะเดียวกัน ปฏิกิริยาของตลาดต่อการตัดสินใจของ Fed ในเดือนกันยายนยังค่อนข้างเบาแน่นอน การคาดการณ์ว่าจะมีการลดอัตราดอกเบี้ยในอนาคตได้ช่วยให้สินทรัพย์เสี่ยงได้ประโยชน์ ดัชนีหุ้น S&P 500, ดาวโจนส์ และแนสแด็ก ต่างก็ปรับตัวสูงขึ้น และคริปโตเคอเรนซีก็แข็งค่าขึ้น ในทางกลับกัน ดัชนีดอลลาร์ (DXY) ลดลง คู่สกุลเงิน EUR/USD ซึ่งเคลื่อนไหวตรงกันข้ามกับดัชนีนี้ ตอนแรกพุ่งขึ้นไปที่ 1.1188 แล้วลดลงไปที่ 1.1080 แสดงความผันผวนรายสัปดาห์สูงสุด 108 จุด จากนั้นความผันผวนเริ่มลดลง คลื่นเริ่มสงบลง และคู่เงินปิดตลาดที่ 1.1162

● ความคิดเห็นของผู้เชี่ยวชาญเกี่ยวกับพฤติกรรมของ EUR/USD ในระยะใกล้มีดังนี้: มีเพียง 20% ของนักวิเคราะห์เท่านั้นที่ลงคะแนนให้ดอลลาร์ แข็งค่าและคู่เงินลดลง 65% ให้คะแนนว่าคู่เงินจะปรับตัวสูงขึ้น และอีก 15% อยู่ในสถานะกลาง อย่างไรก็ตาม เมื่อไปสู่การคาดการณ์ระยะกลาง ภาพจะเปลี่ยนไปอย่างรวดเร็ว ที่นี่ 65% เข้าข้างสกุลเงินสหรัฐฯ โดยคาดว่าคู่เงินจะลดลงต่ำกว่า 1.1000 ผู้สนับสนุนสกุลเงินยูโรในช่วงเวลานี้มีเพียง 20% เท่านั้น ขณะที่อีก 15% ยังคงเป็นกลางไม่ออกความเห็น ในการวิเคราะห์ทางเทคนิคบนกราฟ D1 100% ของตัวบ่งชี้แนวโน้มและออสซิลเลเตอร์เป็นสีเขียว แม้ว่า 1 ใน 4 ของออสซิลเลเตอร์จะส่งสัญญาณว่าอยู่ในภาวะซื้อมากเกินไป แนวรับที่ใกล้ที่สุดสำหรับคู่อยู่ที่ 1.1135-1.1150 จากนั้นที่ 1.1100, 1.1000-1.1025, 1.0880-1.0910, 1.0780-1.0805, 1.0725, 1.0665-1.0680, 1.0600-1.0620 ส่วนแนวต้านอยู่ในโซน 1.1185-1.1200, 1.1275, 1.1385, 1.1485-1.1505, 1.1670-1.1690 และ 1.1875-1.1905

● ในสัปดาห์หน้า พลวัตของคู่สกุลเงินดอลลาร์หลักๆ ได้แก่ EUR/USD, GBP/USD และ USD/JPY อาจได้รับอิทธิพลอย่างมากจากเหตุการณ์ต่อไปนี้ ในวันจันทร์ที่ 23 กันยายน จะมีการเปิดเผยข้อมูลดัชนีผู้จัดการฝ่ายจัดซื้อ (PMI) เบื้องต้นในภาคต่างๆ ของเศรษฐกิจเยอรมนี ยูโรโซน สหราชอาณาจักร และสหรัฐอเมริกา หลังจากหยุดพักจากข่าวเศรษฐกิจสำคัญๆ ในวันพฤหัสบดีที่ 26 กันยายน จะมีการเผยแพร่ข้อมูล GDP ของสหรัฐฯ สำหรับไตรมาสที่สองและจำนวนผู้ขอรับสวัสดิการว่างงานครั้งแรกในประเทศ นอกจากนี้ในวันเดียวกันนี้ยังมีกำหนดการรับฟังรายงานอัตราเงินเฟ้อในรัฐสภาสหราชอาณาจักรและการกล่าวสุนทรพจน์ของประธานธนาคารกลางสหรัฐ เจอโรม พาวเวลล์ และในช่วงท้ายสัปดาห์ทำการ ในวันศุกร์ที่ 27 กันยายน จะมีการเปิดเผยข้อมูลเงินเฟ้อของภูมิภาคโตเกียว (ญี่ปุ่น) นอกจากนี้ ในวันดังกล่าวเราจะได้รับข้อมูลสถิติเงินเฟ้อเพิ่มเติมจากสหรัฐฯ ในรูปของดัชนี Core Personal Consumption Expenditures (PCE) เทรดเดอร์ที่ซื้อขายคู่สกุลเงินเยนควรทราบว่าวันจันทร์ที่ 23 กันยายนเป็นวันหยุดในญี่ปุ่น เนื่องจากประเทศฉลองวันสารทฤดูใบไม้ร่วง

GBP/USD: อัตราคงที่, ปอนด์แข็งค่า

● สัปดาห์ที่แล้วมีการประชุมธนาคารกลางเพิ่มเติมสองแห่ง ได้แก่ ธนาคารกลางอังกฤษ (BoE) ในวันพฤหัสบดีที่ 19 กันยายน และธนาคารกลางญี่ปุ่น (BoJ) ในวันศุกร์ที่ 20 กันยายน ผลจากการประชุมครั้งแรก ทำให้เงินปอนด์อังกฤษเทียบกับดอลลาร์สหรัฐฯ สูงสุดในรอบ 2.5 ปี เหตุการณ์นี้เกิดขึ้นท่ามกลางการตัดสินใจของธนาคารกลางอังกฤษที่จะคงอัตราดอกเบี้ยมาตรฐานไว้ที่ระดับปัจจุบันที่ 5.00% และงดเว้นจากการดำเนินการลดลงอย่างเร่งด่วน ส่งผลให้หลังจากการประกาศการตัดสินใจนี้ คู่สกุลเงิน GBP/USD พุ่งขึ้นสู่ระดับ $1.3339 เป็นครั้งแรกนับตั้งแต่เดือนมีนาคม 2022

● แม้ว่าผลตอบแทนของพันธบัตรรัฐบาลสหราชอาณาจักรจะลดลง แต่ตลาดก็ได้ปรับการคาดการณ์เกี่ยวกับการผ่อนคลายนโยบายการเงินเพิ่มเติมของธนาคารกลางอังกฤษ (BoE) อย่างรวดเร็ว ปัจจุบัน ตามการคาดการณ์ค่ามัธยฐาน การลดอัตราดอกเบี้ยลง 42 จุดพื้นฐานคาดว่าจะเกิดขึ้นภายในสิ้นเดือนธันวาคม เมื่อเทียบกับ 50 จุดพื้นฐานที่คาดการณ์ไว้ก่อนการประชุมครั้งล่าสุด (แม้ว่าจะเป็นการปรับเปลี่ยนที่เล็กน้อยและค่อนข้างมีเงื่อนไข) นักยุทธศาสตร์มหภาคจากกลุ่มธนาคารมิสึโฮ อินเตอร์เนชันแนล เชื่อว่าการลดอัตราดอกเบี้ยจะเกิดขึ้นช้าๆ อาจเป็นรายไตรมาส ในมุมมองของพวกเขา เมื่อพิจารณาจากฉากหลังนี้ GBP/USD มีศักยภาพในการเติบโตต่อไปและอาจทะลุระดับ 1.3400 ได้ในช่วงต้นเดือนตุลาคม โดยคู่สกุลเงินอาจแตะ $1.4000 ภายในสิ้นปี 2025

ด้วยเหตุนี้ เงินปอนด์จึงกลายเป็นสกุลเงินที่ประสบความสำเร็จมากที่สุดในกลุ่มประเทศ G10 ในปีนี้ แม้ว่านักลงทุนจะคาดการณ์ว่านโยบายของธนาคารกลางอังกฤษจะผ่อนคลายในเดือนพฤศจิกายน แต่พวกเขามั่นใจว่าความกดดันด้านเงินเฟ้อในประเทศจะยังคงสูงเพียงพอที่จะรองรับอัตราดอกเบี้ยที่ค่อนข้างสูงเมื่อเทียบกับเศรษฐกิจอื่น ๆ

USD/JPY: อัตราคงที่, เยนอ่อนค่า

● เช่นเดียวกับธนาคารกลางอังกฤษ ธนาคารกลางญี่ปุ่น (BoJ) ตัดสินใจคงอัตราดอกเบี้ยมาตรฐานไว้ที่ระดับเดิมในการประชุมครั้งล่าสุด การตัดสินใจนี้ได้รับการคาดหมายจากผู้เข้าร่วมตลาด อย่างไรก็ตาม ในขณะที่ Fed, ECB และธนาคารกลางอังกฤษมุ่งเน้นไปที่การลดอัตราดอกเบี้ย ตลาดคาดว่าธนาคารกลางญี่ปุ่นจะทำตรงกันข้าม – ปรับขึ้นอัตราดอกเบี้ย อย่างไรก็ตาม ผู้ว่าการ BoJ คาสึโอะ อูเอดะ ระบุในงานแถลงข่าวหลังการประชุมว่าเขาไม่มีแผนที่จะเร่งกระบวนการนี้ อัตราดอกเบี้ยได้รับการปรับขึ้นแล้วในเดือนมีนาคมและกรกฎาคมปีนี้ และตอนนี้เป็นเวลาที่จะหยุดและประเมินผลลัพธ์ที่เกิดขึ้น อูเอดะเน้นว่าธนาคารกลางญี่ปุ่นจะปรับขึ้นอัตราดอกเบี้ยต่อไปหากตัวชี้วัดทางเศรษฐกิจและเงินเฟ้อตรงตามการคาดการณ์ อย่างไรก็ตาม แรงกดดันเงินเฟ้อที่อ่อนลงเนื่องจากค่าเงินเยนที่อ่อนค่าลง ทำให้ธนาคารสามารถใช้แนวทางที่ระมัดระวังมากขึ้นในการตัดสินใจในอนาคต

● หลังจากคำแถลงนี้ เงินเยนญี่ปุ่นขายออกอย่างรวดเร็ว โดยคู่สกุลเงิน USD/JPY แตะระดับสูงสุดที่ 144.49 ฟิวเจอร์สของพันธบัตรรัฐบาลญี่ปุ่นอายุ 10 ปี เพิ่มขึ้นเกือบ 30 จุดพื้นฐาน และดัชนี Topix ซึ่งสะท้อนถึงสภาพตลาดหุ้นของญี่ปุ่นเพิ่มขึ้น 1%

นักวิเคราะห์ทั่วโลกแสดงความคิดเห็นเกี่ยวกับผลกระทบที่อาจเกิดขึ้นจากการตัดสินใจของ BoJ ผู้เชี่ยวชาญจาก Saxo Markets เขียนว่า “ไม่มีความเร่งด่วนในการทำให้ปกติต่อไปจากธนาคารกลางญี่ปุ่น ตราบใดที่อูเอดะยังคงรักษาน้ำเสียงเดิมไว้ หุ้นญี่ปุ่นจะได้รับประโยชน์จากสถานการณ์ที่เกิดจากการลดอัตราดอกเบี้ยอย่างรวดเร็วของ Fed” ในทางกลับกัน Sumitomo Mitsui Bank เชื่อว่าความเป็นไปได้ของการขึ้นอัตราดอกเบี้ยในเดือนธันวาคมยังคงต่ำ เนื่องจากค่าเงินเยนที่อ่อนค่าลงสนับสนุนตลาดหุ้น ซึ่งเป็นการกระตุ้นการเติบโตของค่าแรง

คริปโตเคอเรนซี: “บิทคอยน์ – การลงทุนที่ดีที่สุดในโลก”

● เมื่อเร็วๆ นี้ อาร์เธอร์ เฮย์ส ผู้ร่วมก่อตั้งและอดีต CEO ของ BitMEX ได้เปรียบเทียบผลกระทบของการลดอัตราดอกเบี้ยของ Fed ต่อเศรษฐกิจสหรัฐฯ กับ “ความเมาหวาน” ซึ่งอาจก่อให้เกิดผลกระทบระลอกและการปรับขึ้นอย่างรวดเร็วในระยะสั้น และแล้วอัตราดอกเบี้ยก็ถูกลดลงทันทีถึง 50 จุดพื้นฐาน สินทรัพย์เสี่ยงประสบกับภาวะ "ความสุขชั่วคราว" ที่สัญญาไว้ ดัชนีหุ้น S&P 500, ดาวโจนส์ และแนสแด็ก ต่างพุ่งสูงขึ้นตามมาด้วยสินทรัพย์ดิจิทัล การเรียกว่าการปรับขึ้นแบบพุ่งพรวดหรือการชุมนุมอาจเป็นการพูดเกินจริง แต่ตามที่เฮย์สกล่าวว่า "นี่คือความสงบก่อนเกิดพายุ" “โดยปกติจะเป็นแบบนี้” เขาเขียน “ครั้งแรกจะมีปฏิกิริยาทันที จากนั้นปฏิกิริยาที่แท้จริงจะมาเมื่อปิดตลาดการเงินแบบดั้งเดิมในวันศุกร์ หลังจากนั้นคริปโตเคอเรนซีก็จะติดตามพวกเขา – ขึ้นหรือลง – ในช่วงสุดสัปดาห์” อย่างไรก็ตาม เนื่องจากการทบทวนนี้ถูกเขียนขึ้นในวันศุกร์ เรายังไม่สามารถตรวจสอบความถูกต้องของคำกล่าวของผู้ร่วมก่อตั้ง BitMEX ได้

● ตามที่อาร์เธอร์ เฮย์ส กล่าวไว้ว่า การลดอัตราดอกเบี้ยท่ามกลางการออกเงินดอลลาร์สหรัฐที่เพิ่มขึ้นและการใช้จ่ายของรัฐบาลที่เพิ่มขึ้นเป็นความผิดพลาดสำหรับระบบการเงินทั่วโลก แต่จะทำให้คริปโตเคอเรนซีเป็นที่ต้องการของนักลงทุนมากขึ้น เนื่องจากผลตอบแทนจากการลงทุนของพวกเขาจะเพิ่มขึ้น

ที่ BlackRock ซึ่งเป็นบริษัทจัดการสินทรัพย์ที่ใหญ่ที่สุดในโลก ได้กล่าวว่า แม้ว่านักลงทุนจะวิเคราะห์คริปโตเคอเรนซีได้ยากเมื่อเทียบกับสินทรัพย์แบบดั้งเดิม แต่บิทคอยน์ได้กลายเป็น “แหล่งหลบภัย” สำหรับหลายๆ คนท่ามกลางความตึงเครียดทางภูมิรัฐศาสตร์ที่เพิ่มขึ้น นักวางกลยุทธ์ของ BlackRock ตั้งข้อสังเกตว่าคริปโตเคอเรนซีชั้นนำอาจกลายเป็นเครื่องมือที่มีประสิทธิภาพในการป้องกันความเสี่ยงทางการเงินโลกที่กำลังเกิดขึ้น นอกจากนี้ ตามการพยากรณ์ของพวกเขา เมื่อ BTC ได้รับการยอมรับ “ในฐานะทางเลือกทางการเงินระดับโลก” การเคลื่อนไหวที่สอดคล้องกับหุ้นของบริษัทในสหรัฐฯ และการพึ่งพาอัตราดอกเบี้ยของ Fed จะค่อยๆ ลดลง

● นักกลยุทธ์การลงทุนและผู้เขียนหนังสือขายดี “Broken Money” ลิน อัลเดน เชื่อว่าการนำคริปโตเคอเรนซีมาใช้ในสังคมไม่ใช่เรื่องเร็ว แต่เป็นเรื่องรวดเร็ว และหากบิทคอยน์ยังคงเป็นผู้นำในบรรดาสินทรัพย์ดิจิทัลและถูกมองว่าเป็นที่เก็บมูลค่าที่เชื่อถือได้ ราคาของบิทคอยน์ในอีกสิบถึงสิบเอ็ดปีข้างหน้าอาจสูงถึง $1 ล้านต่อเหรียญ

อัลเดนเห็นด้วยกับการพยากรณ์ของ Cathie Wood CEO ของ Ark Invest ว่าราคาของบิทคอยน์อาจพุ่งสูงถึง $1.5 ล้าน อย่างไรก็ตาม ตามความเห็นของผู้เชี่ยวชาญ ระยะเวลาที่ Wood พยากรณ์นั้นก้าวร้าวเกินไป CEO ของ Ark Invest เชื่อว่าบิทคอยน์จะสูงถึงหกหลักภายในหกปีนับจากนี้ คือภายในปี 2030 อย่างไรก็ตาม อัลเดนเชื่อว่าปี 2035 เป็นวันที่น่าจะเป็นไปได้มากที่สุด

"การไม่ซื้อบิทคอยน์ในขั้นตอนนี้ถือเป็นอาชญากรรม" ผู้เขียน Broken Money กล่าว ตามที่เธอกล่าว "ตอนนี้บิทคอยน์เป็นการซื้อที่ดีที่สุดในตลาดโลก เนื่องจากสินทรัพย์นี้มีศักยภาพในระยะยาว" ลิน อัลเดนมั่นใจว่าในอนาคตบิทคอยน์จะมีมูลค่าสูงกว่าทองคำทางกายภาพ (เพื่อเป็นข้อมูล: มูลค่าตลาดของโลหะมีค่านี้ในปัจจุบันอยู่ที่ประมาณ $17 ล้านล้าน บิทคอยน์ – $1.17 ล้านล้าน ซึ่งต่ำกว่าทองคำถึง 14.5 เท่า)

● ขอให้เราจดจำว่าเมื่อเร็ว ๆ นี้ แจ็ค ดอร์ซีย์ ผู้ร่วมก่อตั้งและอดีต CEO ของทวิตเตอร์ ได้กล่าวในทำนองเดียวกันว่า BTC จะสูงถึง $1 ล้านภายในปี 2030 อย่างไรก็ตาม การพยากรณ์ที่น่าประทับใจที่สุดมาจากผู้ก่อตั้ง MicroStrategy ไมเคิล เซย์เลอร์ ซึ่งระบุว่าบิทคอยน์จะพุ่งขึ้นเป็น 70 (!) เท่าในไม่ช้า – ไปถึง $3.85 ล้าน ในระยะยาว ตามที่เศรษฐีพันล้านคนนี้กล่าวไว้ ทองคำดิจิทัลอาจเพิ่มขึ้นเป็น $13 ล้าน อย่างไรก็ตาม คาดว่าสิ่งนี้จะเกิดขึ้นภายในปี 2045 ภายในปี 2050 มูลค่าตลาดของบิทคอยน์จะเท่ากับ 13% ของทุนทั้งหมดในโลก (ปัจจุบันตัวเลขนี้อยู่ที่ 0.1%)

● กลับมาจากปี 2050 สู่ปี 2024 ให้เราชี้ให้เห็นถึงการพยากรณ์ของผู้ร่วมก่อตั้ง WeRate ควินเทน ฟรองซัวส์ ข้อมูลของเขาระบุว่าการเริ่มต้นของกระทิงกำลังจะเริ่มขึ้น “วัฏจักรบิทคอยน์โดยเฉลี่ยเริ่มต้นประมาณ 170 วันหลังจากการฮาล์ฟ และจุดสูงสุดจะก่อตัวหลังจากผ่านไป 480 วัน” เขาเขียน จากสิ่งนี้ ไม่เหลือเวลาอีกมากก่อนที่การพุ่งขึ้นจะเริ่มขึ้น – การพุ่งขึ้นตามกราฟของควินเทน ฟรองซัวส์ คาดว่าจะเริ่มในวันอังคารที่ 8 ตุลาคม นักวิเคราะห์ยังเชื่อว่าด้วยการตัดสินใจของ Fed เกี่ยวกับอัตราดอกเบี้ย มีความเป็นไปได้ที่ BTC จะพุ่งขึ้นเหนือ $64,500 อย่างรวดเร็ว ด้วยเหตุนี้ ในช่วงเดือนตุลาคม-พฤศจิกายน ราคาอาจเพิ่มขึ้นอย่างน้อย 46% แตะ $90,000-95,000

● การพยากรณ์ในทำนองเดียวกันมาจาก Michael van de Poppe ประธานเจ้าหน้าที่ฝ่ายการลงทุนและผู้ก่อตั้ง MN Trading Consultancy ตามที่เขากล่าว การเติบโตของสภาพคล่องทั่วโลกจะกลายเป็นตัวเร่งที่สำคัญสำหรับวัฏจักรกระทิงครั้งต่อไปในตลาดดิจิทัล “คริปโตเคอเรนซีและสินค้าโภคภัณฑ์มีมูลค่าต่ำมาก” van de Poppe เขียน “และมีความเป็นไปได้สูงที่พวกเขาจะเข้าสู่ตลาดกระทิงเป็นเวลา 10 ปี ฉันคาดว่าจะเห็นการเติบโตอย่างมากจากสินทรัพย์ทั้งสองประเภทนี้” ตามความเห็นของผู้เชี่ยวชาญ คริปโตเคอเรนซีชั้นนำพร้อมที่จะพุ่งขึ้นไปที่ $90,000 แล้ว

ในฐานะระดับการสนับสนุนที่สำคัญสำหรับบิทคอยน์ Michael van de Poppe ระบุที่ $58,000 ความเป็นไปได้ที่ราคาจะลดลงต่ำกว่า $55,000 ตามที่เขากล่าวนั้นแทบไม่มีเลย ควรสังเกตว่าในช่วงต้นเดือนกันยายน นักวิเคราะห์จาก ARK Invest ได้ระบุระดับสำคัญไว้ที่ $52,000 และ $46,000 ในขณะเดียวกัน ควินเทน ฟรองซัวส์ จาก WeRate ซึ่งกล่าวถึงข้างต้น เชื่อว่าสำคัญที่สินทรัพย์จะรักษาตำแหน่งเหนือโซนสำคัญที่ $59,000

● การผ่อนคลายน โยบายการเงินของ Fed และธนาคารกลางอื่นๆ ควรช่วยเหลือ altcoins ด้วยเช่นกัน ตามที่นักวิเคราะห์ วลาดิเมียร์ โคเฮน กล่าวไว้ สภาพคล่องเริ่มออกจากภาคส่วนนี้ในเดือนเมษายน ซึ่งทำให้ความกลัวเข้าครอบงำในช่วงฤดูร้อน อย่างไรก็ตาม เทรนด์ได้เปลี่ยนไปแล้ว และการไปถึงจุดสูงสุดของมูลค่าตลาด $1.1 ล้านล้านนั้นเป็นเพียงเรื่องของเวลาเท่านั้น คาดว่าจะมีสภาพคล่องจำนวนมากไหลเข้าสู่ตลาดนี้เนื่องจากนโยบายของธนาคารกลางที่ผ่อนคลายลง นอกจากนี้ ตามที่ผู้เชี่ยวชาญกล่าวไว้ altcoins บางตัวจะแสดงการเติบโตเป็นพันเปอร์เซ็นต์ ในขณะที่ตัวอื่นๆ จะตายในที่สุด โคเฮนเชื่อว่าการนำเหรียญที่ไม่ให้คุณค่าที่แท้จริงออกไปจะมีบทบาทในเชิงบวก เนื่องจากจะทำให้กลุ่มนี้มีความโปร่งใสและมีสภาพคล่องมากขึ้น

● วลาดิเมียร์ โคเฮน ยังตั้งข้อสังเกตว่า เจ้าของ altcoins ในปัจจุบันได้เปลี่ยนมาใช้กลยุทธ์การถือครองในระยะยาว โดยพร้อมที่จะทนต่อการลดลงของมูลค่าในระยะสั้น ในขณะที่คาดหวังการปรับขึ้นในอนาคต แนวโน้มที่คล้ายกันกำลังเกิดขึ้นกับบิทคอยน์โดยนักวิเคราะห์ที่ CryptoQuant อุปทานบิทคอยน์ที่มีอยู่กำลังลดลงเนื่องจากผู้ใช้ถอนเหรียญออกมาเพื่อการถือครองในระยะยาวโดยไม่ตั้งใจที่จะขาย "แรงกดดันในการขายกำลังลดลงเนื่องจากมีเหรียญน้อยลงสำหรับการซื้อขาย ผู้ค้าบางรายกำลังฝากเงินเข้ากองทุนอนุพันธ์เพื่อเปิดสถานะระยะยาว โดยเดิมพันว่าราคาจะปรับตัวสูงขึ้น" นักวิเคราะห์ของ CryptoQuant เขียน อย่างไรก็ตาม พวกเขายังเชื่อว่าราคา BTC ไม่น่าจะมีการเปลี่ยนแปลงอย่างมีนัยสำคัญในระยะสั้น

● ณ เวลาที่เขียนบทความนี้ ในช่วงเย็นของวันศุกร์ที่ 20 กันยายน หลังการประชุมของ Fed สหรัฐฯ คู่สกุลเงิน BTC/USD ปรับตัวสูงขึ้นและมีการซื้อขายอยู่ที่ประมาณโซน $62,840 มูลค่าตลาดรวมของคริปโตเคอเรนซีเพิ่มขึ้นเล็กน้อยเป็น $2.19 ล้านล้าน (เมื่อเทียบกับ $2.10 ล้านล้านเมื่อสัปดาห์ที่แล้ว) ดัชนี Crypto Fear & Greed ก็เพิ่มขึ้นจาก 32 เป็น 54 จุด โดยย้ายจากโซนความกลัวไปยังโซนเป็นกลาง

กลุ่มวิเคราะห์ NordFX

ข้อจำกัดความรับผิดชอบ: วัสดุเหล่านี้ไม่ใช่คำแนะนำการลงทุนหรือแนวทางในการทำงานในตลาดการเงิน และมีไว้เพื่อวัตถุประสงค์ในการให้ข้อมูลเท่านั้น การซื้อขายในตลาดการเงินมีความเสี่ยงและอาจทำให้สูญเสียเงินที่ฝากไว้ทั้งหมด