EUR/USD: ドル高背景理由

● 先週のマクロ経済統計に関しては、特に乏しかったため、市場関係者のセンチメントはダボス会議(WEF)での発言に大きく左右されました。この会議は、毎年スイスのスキーリゾートで開催され、120ヵ国以上の世界のエリートの代表が集まります。太陽の光を浴びてキラキラと輝く透き通った雪の中、世界の権力者たちは経済問題や国際政治について討議します。今年で、このフォーラムは54回目となり、1月15日‐19日に開催されました。

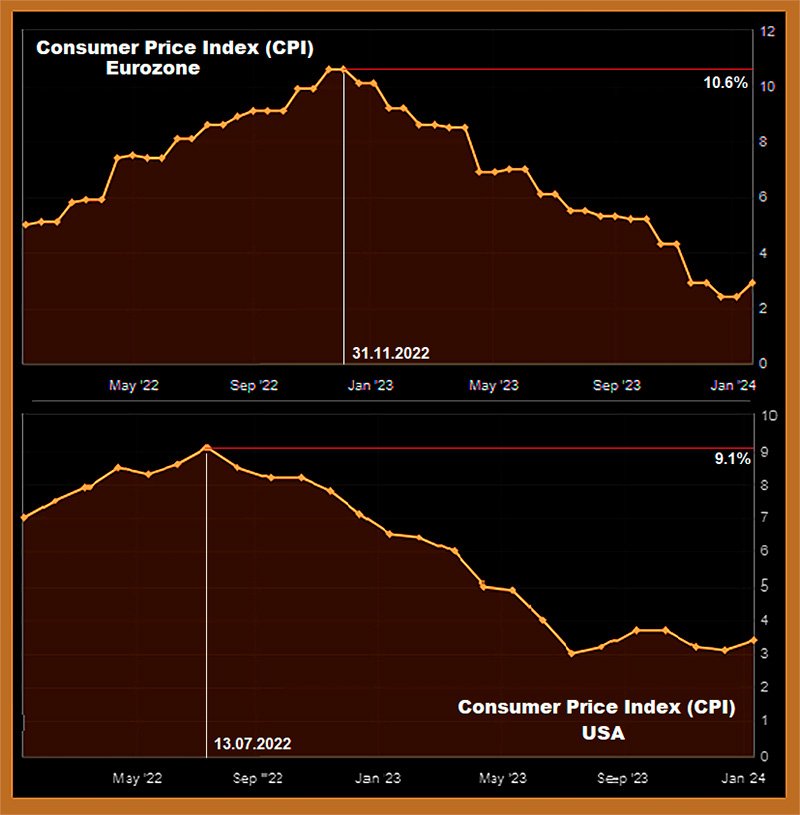

● 1月16日の世界経済フォーラムで講演した欧州中央銀行のクリスティーヌ・ラガルド総裁はインフレ率が目標水準の2.0%に到達する自信を表明しました。ユーロ圏の消費者物価指数(CPI)が着実な低下を示していることから、この発言には何の疑問もありませんでした。CPIは2022年末の10.6%の水準から現在は2.9%まで低下しました。ECB理事会メンバーのイザベル・シュナーベル氏は、欧州経済のソフトランディングと2024年末には目標インフレレベルに戻ることを否定しませんでした。

ロイターが今後のECBの金融政策について有数のエコノミストに調査を実施したところ、ECBが早ければ第2四半期にも利下げに踏み切るとの見方が大半を占めており、45%が6月の金融政策決定会合で利下げ決定されると回答しています。

● 一方、米国のインフレ率は2023年7月以降、3.0%の大台を切ることができません。1月11日に発表された数字によると、年間消費者物価指数(CPI)は3.4%に上昇、コンセンサス予想の3.2%、前回の3.1%を上回りました。月ベースでも、消費者物価指数は予想の0.2%と前回 0.1%に対して 0.3%を記録しました。

このことを踏まえ、また、米国経済がかなり安定していることを考慮すると、連邦準備制度理事会の3月の利下げの可能性は低くなりました。こうした感情の移りで若干のドル高となり、EUR/USD は、1.0900-1.1000圏内から 1.0845-1.0900圏内へと推移しました。 また、アジア株式市場の低迷もユーロにある程度の圧力となりました。

● オランダのラボバンクのエコノミストによると、ユーロのロングポジションはさらなる試練となりそうです。ドナルド・トランプ氏がホワイトハウスで2期目を目指す動きを続ければ、そうなりそうです。“バイデン大統領のインフレ抑制法は、ヨーロッパのこの4年間にとって必ずしも平坦ではなかったが、NATO、ウクライナ、そしておそらく気候変動に対するトランプ氏の姿勢は、欧州にとって負担となり、安全資産としてさらに米ドルのアピールとなる"とロボバンクのエコノミストは著しています。"このことから、EUR/USD の3ヵ月後の見通しでは、1.0500に下落する可能性がある "。

● EUR/USD の先週の終値は1.0897でした。今後の見通しでは、現在アナリストの大半が米ドル高予想です。 60% がドル高、20% が中立です。D1チャートのオシレーター系がアナリスト予想を裏付けています: 80% が赤で弱気トレンドを示しており、20% が中立のグレーです。トレンド系では、赤 (弱気) と緑(強気)で50/50に分かれています。

直近のサポートレベルは、1.0845-1.0865に続いて、1.0725-1.0740、1.0620-1.0640、1.0500-1.0515、 1.0450です。上昇すれば、強気筋は1.0905-1.0925、1.0985-1.1015、 1.1110-1.1140、 1.1230-1.1275、1.1350、 1.1475でレジスタンスに直面します。

● 先週と違い、来週はかなり統計発表があります。1月23日(火)はユーロ圏の銀行貸出調査が発表されます。1月24日(水)はドイツ、ユーロ圏、米国経済の各部門の生産者物価指数(PPI)が発表されます。メインイベントは、間違いなく1月25日(木)の欧州中央銀行理事会の金利決定です。金利は現行の4.50%水準の据え置き予想です。そのため、投資家は、その後の記者会見での発言に注目します。参考までにですが、連邦準備制度のFOMC会合は1月31日に予定されています。 また、1月25日は米国のGDPと失業率のデータ、翌日は、米国内の個人消費支出が発表されます。

GBP/USD: 高水準のインフレ率が金利高とポンド高をもたらす

● 米国やユーロ圏と異なり、先週のイギリスでは重要な統計がかなりありました。1月17日(水)にトレーダーは12月のインフレデータに注目しました。データによると、消費者物価指数(CPI)は前月比-0.2%から0.4%(コンセンサス予想0.2%)に上昇、前年同月比は4.0%(前回値3.9%、予想3.8%)でした。コアCPIは、変わらずの前年比5.1%でした。

インフレ率上昇が示された報告書が発表された後、イギリスのリス・スーナク首相は市場を落ち着かせるために迅速に行動しました。首相は、インフレ率を11%から4%まで低下させた政府の経済計画が依然として正しく、継続していくと述べました。スーナク首相は、この5ヶ月間の国内賃金率が物価上昇率を上回っており、インフレ圧力が弱まる傾向は今後も続くとも述べました。

● この楽観的な発言にもかかわらず、多くの市場関係者はイングランド銀行(BoE)が金融緩和政策の開始が年末まで延期になる予想しています。コメルツ銀行のエコノミストは、"最新のインフレデータにより、ディスインフレプロセスの鈍化懸念が高まっている" 、"市場はおそらくイングランド銀行がこれを受けて、最初の利下げをより慎重に判断するだろう"と著しました。

イングランド銀行が金融緩和を急がなければ、長期的なポンド高にとって理想的な条件が整うことは明らかです。この見通しにより、GBP/USD は、1月17日に5週連続の下落の流れから1.2596で反転、この流れの中間点である1.2714まで上昇しました。

●GBP/USD が上昇を続ける可能性はかなり大きいものでしたが、19日の今週の取引の最終日に発表されたイギリスの小売売上高の低さが妨げとなりました。データによると、この指標は11月の+1.4%から4.6%に減少、12月は-3.2%でした(予想では-0.5%)。1月24日に発表される製造業とサービス部門の購買担当者景気指数が同様の結果となった場合、ポンドにさらに圧力がかかります。イングランド銀行は、厳格な金融政策が景気を過度に減速させることを恐れ、金融緩和を検討するかもしれません。ING (Internationale Nederlanden Groep)のアナリストによると、政策金利を100 ベーシスポイントまで引き下げれば、GBP/USD は、1-3ヶ月の間に1.2300 下落する見込みです。

ING のアナリストは、3月6日に発表されるイギリス予算が減税課題と共にポンドに大きな影響を与える見方もしています。"2022年9月と異なり" 、"これは債務返済コストの削減で賄われると見られている実質的な減税で、今年のイギリスのGDPは0.2-0.3%が上乗せとなり、イングランド銀行の金利上昇の長期化につながる可能性がある"とアナリストは著しています。

● GBP/USD の先週の終値は1.2703でした。今後数日の見通しでは、65%がこのペアの下落を支持、 25%が上昇支持、そして、10% が中立の立場になります。アナリストの意見とは対照的に、D1のトレンド系では、ポンド支持です: 75% がこのペアの上昇を示しているのに対して、下落は25%。オシレータ系では、 25%がポンドを支持、同数の比率 (25%)でドルを支持、 50% が中立です。このペアが下落すれば、サポートは1.2650、 1.2595-1.2610、1.2500-1.2515、1.2450、1.2330、1.2210、1.2070-1.2085となるでしょう。上昇した場合、 1.2720、1.2785-1.2820、1.2940、1.3000、 1.3140-1.3150が、このペアのレジスタンスとなるでしょう。

● 来週は、先に述べたイベント以外のイギリス経済関連の重要な発表予定はありません。イングランド銀行の次回会合は、2月1日(木)に予定されています。

USD/JPY: '月へのミッション' は継続

●日本の統計局が1月19日(金)に発表したデータによると、12月の全国消費者物価指数(CPI)は前年同月比2.6%となり、11月の2.8%から低下しました。生鮮食品を除く12月の全国消費者物価指数(CPI)は前年同月比2.3%で、前月の2.5%から低下となりました。

インフレ率がすでに低下していることを考えると、疑問が生じます: なぜ、利上げをするのか? 論理的な回答: 不要ということです。これが、市場のコンセンサス予想が、日本銀行(日銀)の1月23日(火)の会合で金利を据え置き、マイナス0.1%の水準の維持を示唆している理由です(日銀の前回の利下げが、200ベーシスポイント引き下げた8年前の2016年1月であることを知っておきましょう)。

● いつも通り、日本の鈴木俊一財務大臣は金曜日に口先介入をまたしましたが、いつも通り、目新しい発言はありませんでした。"為替の動きを注視している"、 "為替市場の動きはさまざまな要因によって決定される" 、"為替はファンダメンタルズ指標に反映して安定的に動くことが重要だ": 市場関係者、このような発言を度々聞かされてきました。もはや、日本の金融当局が説得から実際の行動に移すとは思っていません。そのため、円安が続き、USD/JPY は上昇の動きを続けています(興味深いことに、これは2週間前にお伝えした波動分析とまさに一致)。

●USD/JPY の先週の高値は148.80で、終値は、この水準に近い148.14でした。直近の見通しでは、アナリストの50% がドル高予想、30% が円高予想、20%が中立です。D1のトレンド系とオシレーター系 共に100%が上昇を示しいますが、オシレーター系の4分の1が買われ過ぎ圏内です。直近のサポートは、147.65 に続き、146.90-147.15、146.00、145.30、143.40-143.65、142.20、141.50、 140.25-140.60となります。レジスタンスは次のとおりとなっています: 148.50-148.80、149.85-150.00、150.80、 151.70-151.90。

● 日本銀行の会合以外に日本経済関連のもう一つ重要な来週のイベントとしては、1月26日(金)に予定されている東京都区部消費者物価指数(CPI)の発表があります。

暗号資産: 多くの予想、疑わしい結果

●先週の1月10日、米証券取引委員会(SEC)は予想通り、待ちわびていたビットコインを基にした上場投資信託(ETF)の申請11件を全て一括承認しました。当初、このニュースは、ビットコインを$49,000前後にまで急騰させました。しかし、その後、ビットコインは約15%にもなる$41,400に下落しました。アナリストは、買われ過ぎの状況、いわゆる、"市場の過熱"を ビットコインの下落理由として挙げています。コインテレグラフが報じているように、SECの前向きな決定は既に市場価格に織り込み済みでした。2023年のビットコインは2.5倍に上昇しており、ETFの承認をほぼ避けられなくなった秋に、この上昇のかなりを占めています。多くのトレーダーや投資家、特に短期投機家は、高くなった資産を購入するよりも利確の決定を下しました。これは、"噂(期待)で買い、事実で売る"という相場格言の典型的な例です。

● この暴落は予想外とは言えません。SECの決定に先立ち、一部のアナリストは下落を予測していました。例えば、CryptoQuant のアナリストは、$32,000の下落の可能性を述べていました。ほかの予想では、$42,000 や $40,000のサポートレベルについて言及していました。 "ビットコインは$50,000水準を突破できなかった "、"ビットコインが失った勢いを取り戻せるかが課題となる" とスイスブロックのアナリストは著しています。

● 前回のレビューは、"Xデイは到来。次はどうなる?"でした。ビットコインETFの承認から1週間以上が経過しましたが、BTC/USDのチャートから判断すると、市場はまだこの問いの答えを出していません。MNトレーディング・コンサルタンシー代表のマイケル・ヴァン・デ・ポッペ氏によると、相場はいくつかの段階で伸び悩みます。$46,000は抵抗線ですが、ビットコインは$37,000 と$40,000の間のサポートを試す可能性があります。確かに、先週のビットコインは、横ばい: $42,000 から$43,500の推移でした。しかし、1月18日‐19日のビットコインは、新たな弱気筋に攻撃され、直近安値の$40,280をつけました。

●ビットコイン現物ETFの開始の影響を評価するには、ある程度の時間が必要になります。分析に適したデータが集まるのは2月中旬ごろになる見込みです。しかし、コインテレグラフで指摘しているように、これらのファンドには既に12億5000万ドル以上の資金が集まっています。初日だけでも、この新しい金融商品の取引高は46 億ドルに達しました。

投資銀行モルガン・スタンレーのデジタル資産部門責任者、アンドリュー・ピール氏は、これらの新商品への毎週の資金流入がすでに数十億ドルを超えていると指摘しています。同氏は、ビットコイン現物が世界経済のドル離れを大幅に加速させる可能性があると考えています。"これらのイノベーションはまだ初期段階にあるが、ドル主導に挑戦する機会を与えている。巨大投資家は、独自の特徴と普及が広がっているデジタル資産がドルの今後をどのように変えていくか検討すべきである"と述べました。アンドリュー・ピール氏は、BTC の人気がこの15年間に確実に高まっており、世界で1億600万人以上がビットコインを保有していることを思い出させてくれています。 一方で、マイケル・ヴァン・デ・ポッペ氏は、1月10日の出来事が世界中の多くの人々の生活を変えるだろうと述べています。しかし、同氏は、"これがビットコインなどの暗号資産にとって最後の'簡単な'サイクル になるだろう"、つまり、"以前より時間がかかることになる"と警告しています。

● 新たにスタートしたビットコインETFが世界秩序に与える影響についても、権力ピラミッドの頂点に立つ多くのインフルエンサーの間で話題となっており、この出来事の重要性が浮き彫りになっています。例えば、米国上院銀行委員会のメンバーであるエリザベス・ウォーレン氏は、SECの決定を批判しており、既存の金融システムと投資家に弊害を及ぼす可能性があると懸念を表明しました。対照的なのが、国際通貨基金(IMF)のクリスタリナ・ゲオルギエヴァ専務理事の見解です。専務理事は、暗号資産は通貨ではなく資産であり、これを区別することが重要であるとした見方をしています。したがって、ビットコインがドルの代わりとなることはないと主張しています。また、ビットコインETFがビットコインの大きな普及に貢献すると期待する人々の考えにも賛同していません。

● 分析会社Fundstratの共同設立者であるトム・リー氏はCNBCとのインタビューで、ビットコインの価格が2024年末までに$100,000 - $150,000 、今後5年間で$500,000 になると語っていました。"今後5年間、供給は限られるだろうが、ビットコイン現物ETFが承認されたことで、需要が大きくなる可能性があるため、$500,000 前後になる可能性はかなりあると思う" とリー氏は述べていました。また、さらなる上昇要因として、2024年春に予定されている半減を強調していました。

アーク・インベストのキャシー・ウッドCEOもCNBCで、ビットコインが2030年までに150万ドルになるという強気のシナリオの予測を語っていました。こちらの事務所のアナリストは、ビットコインの価格が少なくても$258,500には上昇すると計算しています。

もう一つの予想は、スカイブリッジ・キャピタルの創設者で元ホワイトハウス広報部長のアンソニー・スカラムッチ氏のものです。"半減期にビットコインが$45,000 だとすると、2025年の半ばには、$170,000になる。4月の半減期のビットコインの価格がどうであれ、4倍にすれば、今後18 ヶ月以内にはその数字になるだろう"と世界経済フォーラムに先立ちダボスでスカイブリッジ・キャピタルの創設者は述べていました。

● 2024年12月31日までのビットコイン価格について、いろいろなAIチャットボットの予想がさまざまなのは興味深いところです。Anthropic のClaude Instant が$85,000の予想をしているのに対してInflection のPi の予想は$75,000の上昇です。Gemini のBardのBTCの予想価格は、$90,000越えですが、不測の経済的障害により、ピークは$70,000が上限と警告しています。OpenAIの ChatGPT-3.5では、$75,000から $85,000 が妥当としていますが保証はしていません。より控えめな予想のChatGPT-4 では、潜在的な市場変動と投資家の警戒を考慮して$40,000 から $60,000を示していますが、$80,000の上昇も否定していません。最後に、Co-Pilotの Bing AIでは、情報収集を基に$75,000前後を予測しています。

AI システムのこのようなさまざまな予測は、暗号資産の相場予想における不確実性と複雑性を反映しており、今後数年間の市場動向に影響を与える可能性のあるさまざまな要因を浮き彫りにしています。

●1月19日の晩時点のBTC/USD は$41,625前後で取引されていました。暗号資産市場の時価総額は1兆6400億ドルとなり、1週間前の1兆7000億ドルから減少しました。市場センチメントを測るビットコインFear & Greed指数では、1週間で71 から 51 ポイントに下がり、'貪欲' 圏内から'中立' 圏内へと移りました。これは暗号資産市場における投資家のより慎重なアプローチに反映した投資家感情の変化を示しています。

● イーサリアムを対象とした現物ETFの開始が差し迫っているという市場の憶測の高まりに関する結論について、前回のレビューではSECのゲーリー・ゲンスラー委員長の発言から規制当局の前向きな決定は、ビットコインに基づく上場商品にのみ適用されることが明らかとなりました。ゲンスラー委員長によれば、この決定は、"証券とみなされる暗号資産の上場基準を承認する準備が整ったことを示すものではない" とのことです。規制当局が商品としてビットコインのみを分類している一方、"暗号資産のほとんどが投資契約(すなわち、有価証券)とみなされている"ことが重要です。

現在、投資銀行TDコーウェンのアナリストらは、ETH ETFに対する悲観論を認めています。同行の情報を基にすると、2024年前半にこの投資商品の申請審査を始める可能性は低そうです。" ETH-ETFの承認前にSECは、 ビットコインの同様の投資商品で実務経験を積みたいと考えているだろう"とT.D. コーウェン ワシントンリサーチグループの責任者であるジャレット・サイバーグ氏はコメントしています。TDコーウェンは、 SECがイーサリアムETFの議論を再検討するのは、2024年11月の米大統領選挙の後だと考えています。

JPモルガンのシニアアナリストであるニコラオス・パナギルツォグロウ氏も、現物ETH-ETFがすぐに承認されるとは考えていません。同氏は、SECが決定を下すには、イーサリアムを証券ではなくコモディティとして分類する必要があるとの見解を示しています。しかし、JP モルガンはそのような展開になる今後の可能性は低いと考えています。

NordFX Analytical Group

注意: この内容は金融市場への投資推奨やガイドラインではなく情報提供のみを目的としています。金融市場の取引には、リスクが伴うため入金した資金のすべてを失う可能性もあります。

戻る 戻る