Pasar utama mengakhiri minggu dengan nada hati-hati, sedikit menghindari risiko. Risalah dari pertemuan terakhir Federal Reserve mengonfirmasi bahwa pengetatan kuantitatif kemungkinan akan berakhir pada awal Desember dan menunjukkan pembuat kebijakan masih terpecah mengenai apakah akan memberikan pemotongan suku bunga lagi pada pertemuan Desember. Perdebatan ini terjadi di tengah data aktivitas yang tangguh: survei bisnis awal untuk November menunjukkan ekspansi yang berkelanjutan di AS, sementara indikator zona euro tetap sedikit di atas ambang batas 50,0 tetapi masih menyoroti kelemahan manufaktur.

Gambaran makro hingga akhir November adalah pertumbuhan global yang stabil tetapi tidak merata. Di Amerika Serikat, pasar menunggu data berikutnya tentang revisi PDB Q3, pendapatan dan pengeluaran pribadi, serta inflasi untuk memperjelas seberapa cepat kebijakan moneter mungkin akan dilonggarkan pada 2026. Di Kanada, inflasi Oktober telah mendekati kisaran target bank sentral, menambah kesan bahwa puncak suku bunga kebijakan sudah berlalu. Bersama dengan angka perumahan dan kepercayaan AS yang akan dirilis dalam beberapa hari mendatang, rilis ini akan membantu membentuk ekspektasi untuk keputusan Fed Desember pada saat pasar masih memperkirakan kemungkinan pemotongan lain yang signifikan, tetapi tidak lagi satu arah.

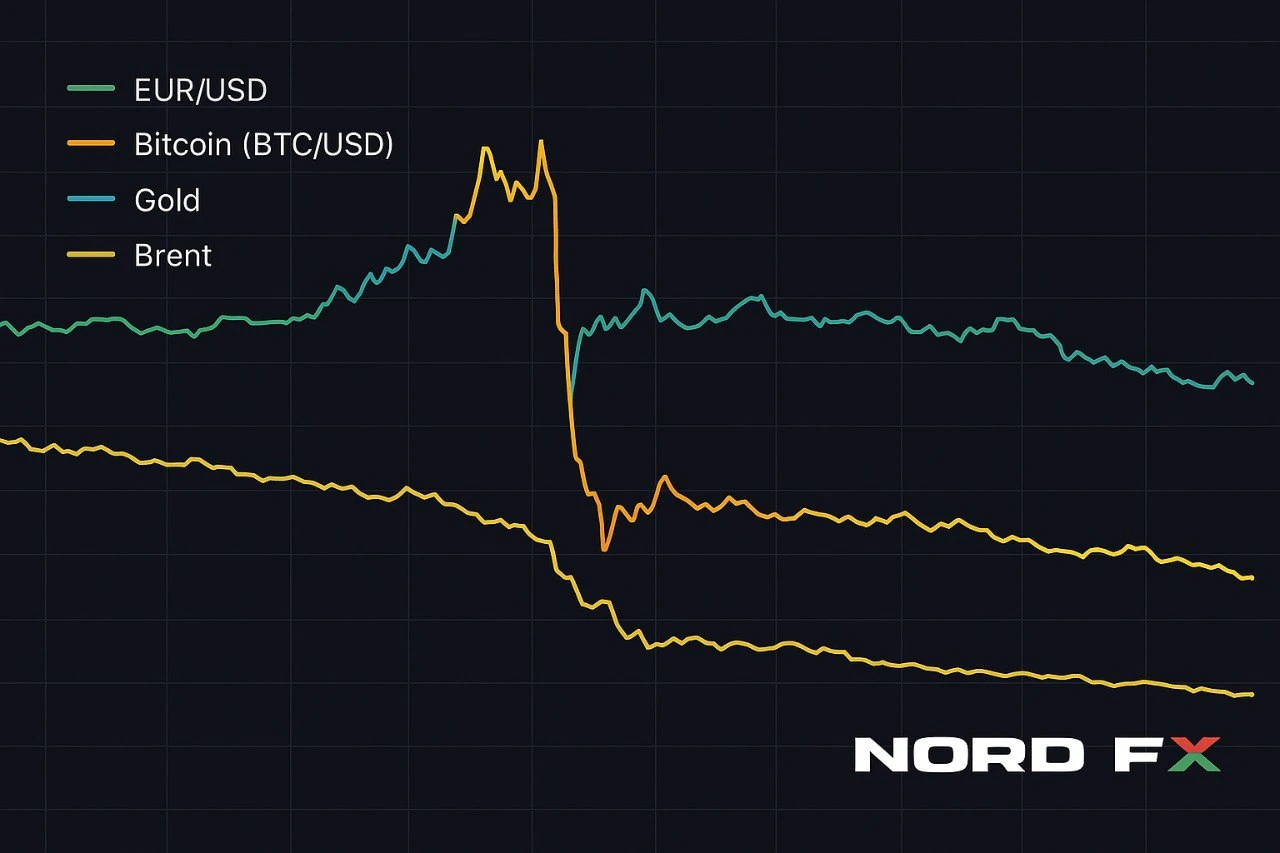

Di tengah latar belakang ini, EUR/USD kembali turun menuju pertengahan 1,15 dan mengakhiri Jumat di 1,1513, setelah diperdagangkan antara 1,1490 dan 1,1553 selama sesi. GBP/USD menutup minggu di sekitar 1,31 setelah bergerak dalam kisaran 1,3040–1,3110. Emas mengkonsolidasikan sedikit di bawah level tertinggi baru-baru ini, dengan harga spot mendekati 4.066–4.080 dolar per ons pada penutupan Jumat. Minyak mentah Brent telah mundur ke kisaran rendah 60-an, mengakhiri minggu mendekati 62,5 dolar per barel. Pasar cryptocurrency tetap di bawah tekanan berat karena bitcoin diperdagangkan di pertengahan 80.000-an dan berada di jalur untuk bulan terburuknya sejak 2022.

Secara keseluruhan, minggu 24–28 November kemungkinan akan didorong oleh data AS yang masuk, komentar baru dari pejabat Fed, dan bagaimana selera risiko berkembang setelah penurunan tajam dalam aset beta tinggi seperti cryptocurrency.

EUR/USD

EUR/USD menghabiskan sebagian besar minggu lalu diperdagangkan di sekitar wilayah 1,15–1,16. Intraday pada hari Jumat, pasangan ini sempat bergerak lebih tinggi menuju 1,1550 menjelang data zona euro, tetapi pembacaan aktivitas bisnis AS yang lebih kuat dari perkiraan dan imbal hasil AS yang kuat kemudian mendorongnya kembali turun. Pada penutupan, EUR/USD berada di 1,1513, dengan tertinggi hari itu di 1,1553 dan terendah di 1,1490, meninggalkan dolar sedikit lebih kuat pada minggu ini.

Di sisi zona euro, PMI komposit flash November tetap sedikit di atas angka 50, menunjukkan ekspansi yang berkelanjutan, tetapi komponen manufaktur telah merosot lebih dalam ke dalam kontraksi dan indikator ketenagakerjaan lemah. Sebaliknya, survei AS menunjukkan gambaran yang agak lebih kuat, terutama di sektor jasa. Latar belakang pertumbuhan dan imbal hasil relatif oleh karena itu masih mendukung dolar pada margin, terutama sementara inflasi zona euro mendekati target ECB dan bank sentral memberi sinyal jeda yang berkepanjangan daripada pelonggaran yang akan datang.

Secara teknis, EUR/USD tetap berada dalam kisaran konsolidasi luas yang telah ada sejak akhir musim panas. Area 1,1490–1,1470 sekarang mewakili zona dukungan kunci terdekat, karena bertepatan dengan terendah hari Jumat dan batas bawah dari kisaran jangka pendek. Penembusan yang meyakinkan di bawahnya akan mengekspos band 1,1400–1,1365 dan meningkatkan risiko koreksi lebih dalam menuju palung awal Oktober. Di sisi atas, resistensi awal terletak di zona 1,1620–1,1660, di mana rata-rata bergerak jangka pendek dan garis tren menurun dari tertinggi November bertemu. Penutupan harian di atas 1,1760–1,1800 akan diperlukan untuk menandakan bahwa pasangan ini siap melanjutkan kenaikan jangka panjangnya menuju wilayah 1,20–1,22.

Pandangan dasar: netral dengan sedikit kecenderungan bearish sementara pasangan ini diperdagangkan di bawah sekitar 1,1660. Pemulihan jangka pendek menuju 1,16–1,17 tetap mungkin jika data AS yang akan datang mengecewakan atau jika komunikasi Fed terdengar lebih dovish daripada yang diharapkan pasar, tetapi euro masih rentan terhadap penjualan baru pada angka yang kuat atau penetapan harga ulang lebih lanjut dari peluang pemotongan suku bunga Desember.

Bitcoin (BTC/USD)

Pasar cryptocurrency menyelesaikan November di bawah tekanan intens. Setelah mencetak rekor tertinggi di atas 120.000 dolar pada bulan Oktober, bitcoin telah kehilangan lebih dari sepertiga nilainya hanya dalam beberapa minggu. Menurut beberapa tempat utama, BTC/USD sempat turun ke area 80.000 pada hari Jumat, dengan terendah intraday sekitar 80.700–81.600 dolar, sebelum memulihkan sebagian kerugiannya. Pada akhir hari, diperdagangkan kira-kira di zona 84.000–85.000, dan pada hari Sabtu berfluktuasi di dekat 84.000–84.500 dolar.

Beberapa kekuatan mendorong pergerakan ini. Gelombang likuidasi panjang yang dipercepat dan pengambilan keuntungan setelah tahun yang sangat kuat bertabrakan dengan prospek pelonggaran Fed yang kurang agresif dan penghindaran risiko yang lebih luas. Aliran masuk ke dana yang terkait dengan bitcoin melambat atau berbalik negatif, dan beberapa investor beralih ke uang tunai dan obligasi berkualitas tinggi sekarang karena imbal hasil riil tetap positif bahkan setelah pemotongan suku bunga sebelumnya. Ini telah memperkuat volatilitas di pasar di mana likuiditas telah menipis setelah penjualan tajam bulan Oktober.

Dari perspektif teknis, BTC/USD jelas telah menembus di bawah band dukungan sebelumnya di area 92.000–95.000 dan sekarang diperdagangkan di dalam saluran menurun yang curam. Rata-rata bergerak jangka pendek telah berbalik, dan indikator momentum berada di wilayah oversold tetapi belum menunjukkan divergensi bullish yang meyakinkan. Zona dukungan terdekat sekarang terletak di sekitar 80.000–78.000 dolar, di mana terendah baru-baru ini dan kluster konsolidasi sebelumnya bertepatan. Jika area ini gagal bertahan, target penurunan berikutnya akan berada di kisaran 76.000–72.000, kira-kira sesuai dengan terendah April. Di sisi atas, area dukungan sebelumnya di sekitar 92.000–95.000 telah berubah menjadi resistensi utama pertama. Hanya pergerakan berkelanjutan kembali di atas 100.000–105.000 yang akan menunjukkan bahwa fase korektif berakhir daripada berkembang menjadi pasar bearish yang lebih lama.

Pandangan dasar: netral-ke-bearish sementara bitcoin tetap di bawah band resistensi 92.000–95.000. Pemulihan jangka pendek mungkin terjadi mengingat tingkat kondisi oversold, tetapi untuk saat ini mereka lebih terlihat seperti pantulan korektif dalam tren turun yang lebih luas daripada awal dari reli impulsif baru.

Minyak Mentah Brent

Futures minyak mentah Brent memperpanjang penurunannya minggu lalu. Kontrak bulan depan untuk Januari diperdagangkan di kisaran rendah 60-an, dengan harga saat ini sekitar 62,5 dolar per barel dan kisaran perdagangan baru-baru ini kira-kira antara 61,9 dan 63,1 dolar. Ini meninggalkan Brent mendekati posisi terendah dari pergerakan saat ini dan turun secara signifikan dari level yang terlihat sebelumnya di musim gugur.

Minyak tetap di bawah tekanan dari kombinasi pasokan yang melimpah, meningkatnya persediaan AS, dan harapan baru untuk kemajuan menuju penyelesaian politik di Eropa Timur, yang akan mengurangi risiko gangguan yang lebih parah terhadap ekspor Rusia. Pada saat yang sama, kekhawatiran permintaan tetap ada karena manufaktur dan perdagangan global terus tertinggal di belakang jasa dan karena suku bunga riil yang relatif tinggi membebani keputusan investasi dan konsumsi.

Secara teknis, Brent masih diperdagangkan di dalam saluran menurun yang luas yang telah ada sejak Q2 2025. Penjual berulang kali muncul di dekat wilayah 66–68 dolar, sementara pembeli masuk mendekati band dukungan 60–61 dolar. Penurunan terbaru telah membawa harga kembali ke setengah bawah dari kisaran ini. Penutupan harian di bawah 61–60,5 dolar akan mengonfirmasi bahwa tekanan bearish meningkat lagi dan dapat membuka jalan menuju 58 dolar dan batas bawah saluran. Di sisi atas, resistensi awal sekarang terletak di dekat 64–65 dolar; hanya penembusan berkelanjutan di atas 68–70 dolar yang akan menandakan bahwa pembalikan bullish yang lebih tahan lama sedang berlangsung dan mengalihkan fokus kembali ke area 74–76 dolar.

Pandangan dasar: netral-ke-bearish sementara Brent diperdagangkan di bawah sekitar 68 dolar per barel. Dengan tidak adanya kejutan pasokan besar, reli menuju resistensi lebih mungkin menarik minat penjualan, terutama jika data yang masuk atau komunikasi Fed menghidupkan kembali kekhawatiran tentang pertumbuhan global yang lebih lambat.

Emas (XAU/USD)

Emas terus berperilaku lebih seperti aset konsolidasi daripada perdagangan tren langsung. Tergantung pada sumber data, spot XAU/USD ditutup pada hari Jumat antara kira-kira 4.066 dan 4.080 dolar per ons, dengan satu seri yang banyak diawasi menunjukkan penutupan di dekat 4.078,5 dolar setelah kisaran sesi sekitar 4.023–4.101 dolar. Hari ini, Sabtu, indikasi perdagangan hanya sedikit lebih rendah, menunjukkan konsolidasi yang sedang berlangsung setelah puncak baru-baru ini di atas 4.300 dolar.

Meskipun ini mewakili penurunan moderat dari level rekor, tren naik yang lebih luas tetap utuh dan keuntungan tahun-ke-tahun masih substansial. Secara fundamental, emas didukung oleh beberapa faktor: inflasi di banyak ekonomi utama tetap di atas target, imbal hasil riil positif tetapi tidak cukup tinggi untuk menghilangkan daya tarik aset lindung nilai, kekhawatiran fiskal di sejumlah negara tetap ada, dan risiko geopolitik tetap tinggi. Pada saat yang sama, perdebatan Fed tentang pelonggaran lebih lanjut membatasi kenaikan dalam jangka pendek, karena nada yang lebih hawkish dari yang diharapkan dapat mendorong lonjakan lain dalam dolar dan imbal hasil riil.

Di grafik, XAU/USD masih diperdagangkan di dalam saluran naik yang luas yang telah berkembang sejak awal 2024. Area 3.980–4.000 dolar sekarang mewakili dukungan penting terdekat, menggabungkan terendah lokal baru-baru ini dengan tepi bawah zona konsolidasi jangka pendek. Penurunan lebih dalam menuju 3.930–3.900 dolar tidak dapat dikesampingkan jika dolar terus pulih atau jika data AS minggu depan datang lebih kuat dari yang diharapkan, tetapi pada level saat ini penurunan seperti itu kemungkinan akan dilihat oleh banyak investor jangka menengah sebagai kesempatan untuk membangun kembali posisi panjang. Di sisi atas, resistensi dikelompokkan antara 4.130 dan 4.180 dolar; penutupan harian di atas area ini akan menunjukkan bahwa fase korektif telah berakhir dan mengalihkan perhatian kembali ke zona rekor sekitar 4.250–4.300 dolar dan mungkin lebih tinggi.

Pandangan dasar: bias beli-saat-penurunan sementara XAU/USD bertahan di atas sekitar 3.900 dolar. Pergerakan signifikan berikutnya kemungkinan akan bergantung pada bagaimana pasar menafsirkan kombinasi data PDB dan inflasi AS dan apakah pesan Fed menggeser ekspektasi untuk suku bunga riil pada 2026.

Kesimpulan

Minggu 24–28 November menemukan pasar di persimpangan penting. Fed telah memberi sinyal akhir yang mendekat untuk pengetatan kuantitatif tetapi belum berkomitmen untuk pemotongan suku bunga lain pada bulan Desember, dan data yang masuk tentang pertumbuhan dan inflasi AS akan memiliki pengaruh yang menentukan pada perdebatan itu. Indikator aktivitas zona euro dan Inggris menunjukkan ekspansi yang berkelanjutan, meskipun sederhana, tetapi wilayah ini tetap sensitif terhadap setiap pengetatan kembali kondisi keuangan global.

Dalam lingkungan ini, EUR/USD terus diperdagangkan di dalam kisaran konsolidasi yang luas, emas berhenti setelah reli yang kuat tetapi masih terlihat didukung pada penurunan, dan Brent tetap dibatasi oleh kekhawatiran tentang permintaan dan normalisasi pasokan. Sementara itu, bitcoin telah mengingatkan para pedagang betapa cepatnya sentimen dapat berbalik dalam aset beta tinggi: koin ini telah mengembalikan sebagian besar keuntungan 2025-nya hanya dalam beberapa minggu karena leverage dan optimisme telah berkurang dan likuiditas telah menipis.

Seperti biasa, pedagang harus tetap fleksibel, memperhatikan tingkat teknis yang disorot di atas dan memantau rilis makro utama dan sinyal bank sentral di hari-hari mendatang. Volatilitas dapat meningkat tajam jika data atau komunikasi Fed secara material mengubah ekspektasi untuk jalur suku bunga dan pertumbuhan global.

Grup Analisis NordFX

Disclaimer: Materi ini bukan rekomendasi investasi atau panduan untuk bekerja di pasar keuangan dan hanya untuk tujuan informasi. Perdagangan di pasar keuangan berisiko dan dapat menyebabkan hilangnya dana yang disetorkan secara keseluruhan.